18 / 40

18 / 40

I

f you use or accept credit or debit cards, this article likely affects you.

In my 20 years of experience with Merchant Services and Credit Card

Processing, I have not seen a more major change than this one. Visa,

MasterCard and others decided a few years ago that having a chip on a

plastic card may reduce fraud that occurs when a bad guy uses stolen

credit and debit card numbers for swiped transactions. These new chip

cards are now coming your way. You need to know the basic facts and

myths about them so customers, fraudsters, and salesmen won’t take off

with your data, your money, or your job.

Why should you care about chip cards?

What does this mean for your Business Office? Will you have to do

anything about this? Yes. No. Maybe.

Here’s the back story:

•

Data thieves are trying to steal credit and debit card info

•

If the thieves win just once, you could lose money, your reputation,

your identity, and maybe your job

•

Reading a special chip on a plastic card can help make stolen card numbers useless

•

This chip-card issue only relates to “swiped” transactions - NOT phone,

mail or internet transactions. Don’t let someone fool you on this point.

So, if your Business Office only accepts mail, phone, and internet

transactions, don’t just blow this off. You will want to know about this

major policy change.

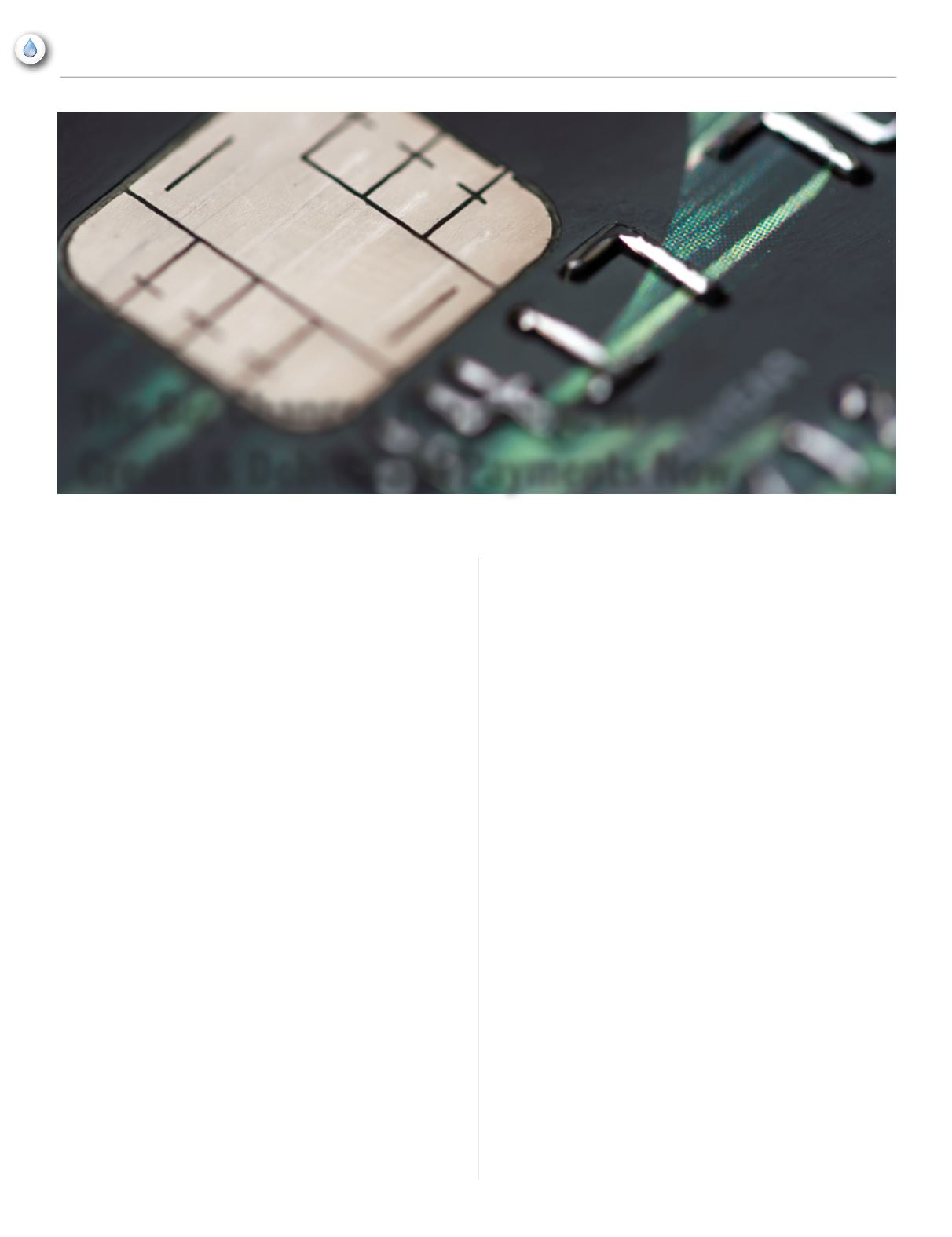

What is a chip card?

The formal name is EMV, which stands for Europay MasterCard

Visa. These cards are the same size and shape as credit and debit

cards you are used to, except they have a metal chip on the front

above the first four digits of your card number. This chip is

activated only when inserted into a certain kind of card-reading

terminal. When this chip is active inside the card terminal, it

creates a one-time-use code that goes along with your card number

and amount of your transaction. This one-time-use code will

not be usable again.

How does a chip card stop fraud?

If a bad guy steals your card number, he won’t have your metal chip

to make the special code. If he steals your card during that specific

transaction, that one-time-use code won’t work again. This should help

data thieves decide to move on to easier targets – and cut down on fraud

at “swiped” points of sale.

No extra fees

Good news here. Customers won’t have any extra fee to use a chip card,

nor will you to accept a chip card at your office.

October 1 Fraud Liability Shift

As of October 1

st

, Visa and MasterCard wanted every consumer to have

a chip on their credit or debit card. They also hoped that every business

that swipes would be able to read these chip cards. That may have been

dreaming, since there were only about 20% of debit cards and 60% of

credit cards that had chips on October 1st – and some say that is an

optimistic estimate.

In my work with Utility Business Offices, I have seen that most card

payments are done with debit or check cards – and most of those

payments are not even “swiped” payments. (The rest of these are

mail, phone, or online payments.) So, your chance of seeing one of

these chips walk in your office may be pretty low for a while yet.

The reason? Money. Plain, non-chip cards cost about $1 to produce

and deliver. Chip cards cost about $10. Wow. Ten times the cost.

And there isn’t a lot of margin in the card business to pay for this.

16

NCRWA.COM|

Fall 2015

feature

The Big Changes Happening in

Credit & Debit Card Payments Now

By Robert Mohon